March 2026 Market Insights

A reading of the month's transactions — and what they tell us about where Jeddah is, and where it is going.

In a single month, more than two billion riyals moved through the Jeddah real estate registry. Nine hundred and eighty-four transactions; 525 land parcels; 456 apartments; a handful of villas and built properties. Read at that altitude, March 2026 looks like an ordinary month in an active market.

Read more closely, it is something else entirely.

In the same city, in the same thirty-one days, residential land changed hands at SAR 11 per square metre — and at SAR 19,800. That is a spread of nearly six thousand to one. It is the most important figure in the brief, and it does not appear in any headline.

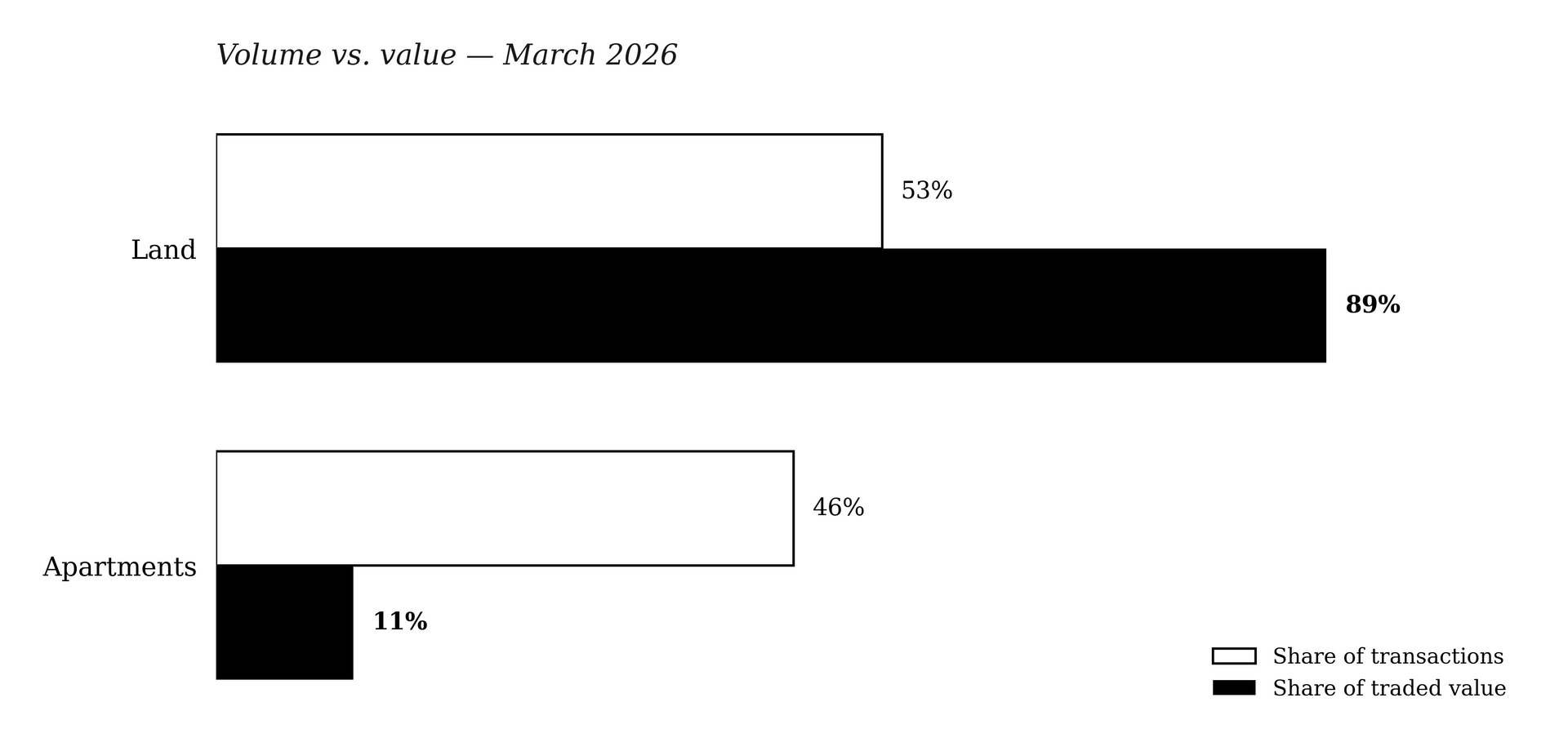

The shape of the month

Total registered value in Jeddah for March stood at approximately SAR 2.41 billion. The composition is instructive: by volume, the market split almost evenly between land and apartments. By value, land accounted for roughly 89 percent of every riyal that changed hands. Apartments — 46 percent of registrations — represented only 11 percent of total value.

This asymmetry is structural, not seasonal. It is in land that institutional capital, developers, and family offices transact. The apartment registry, broader in volume, addresses a different audience entirely.

A single transaction tells the rest of the story. An 86,085-square-metre commercial land parcel in Al Zahra, registered at SAR 600 million, accounted on its own for one quarter of the entire month's traded value. Jeddah, in March, was not a market characterised by uniform activity. It was a market in which a small number of significant decisions moved the dial, while a much larger volume of routine transactions populated the registry around them.

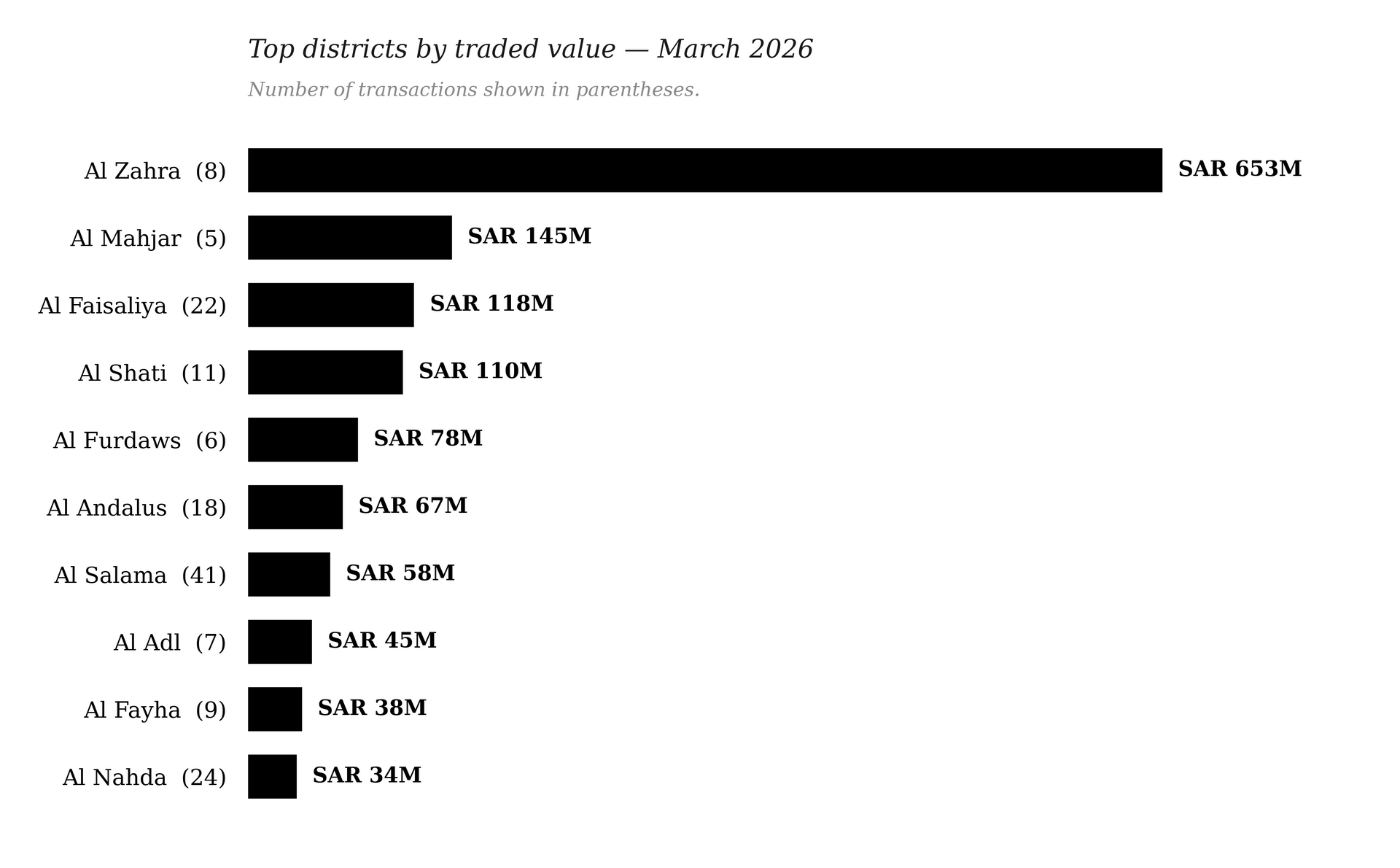

Where the capital concentrated

The geography is unmistakable. The western and northern corridors — Al Zahra, Al Faisaliya, Al Shati, Al Andalus, Al Salama, Al Fayha, Al Nahda — collectively absorbed the majority of capital deployed during the month.

Two patterns sit beneath the totals. The first is the dominance of

commercial land at

strategic scale

— large parcels in Al Zahra, Al Mahjar, Al Shati, and Al Faisaliya, transacting in tranches between thirty and six hundred million riyals. These are the deals that define corporate, institutional, and family-office activity, and they cluster in commercial-zoned land along development corridors aligned with Vision 2030 infrastructure.

The second is the persistence of

ultra-prime residential pricing on Al Shati. A 1,143-square-metre residential parcel that traded at SAR 19,800 per square metre — SAR 22.6 million in absolute terms — is the single most important benchmark for high-net-worth residential intent in Jeddah. It is an order of magnitude above the city-wide average and is the figure against which truly prime Jeddah land should be measured.

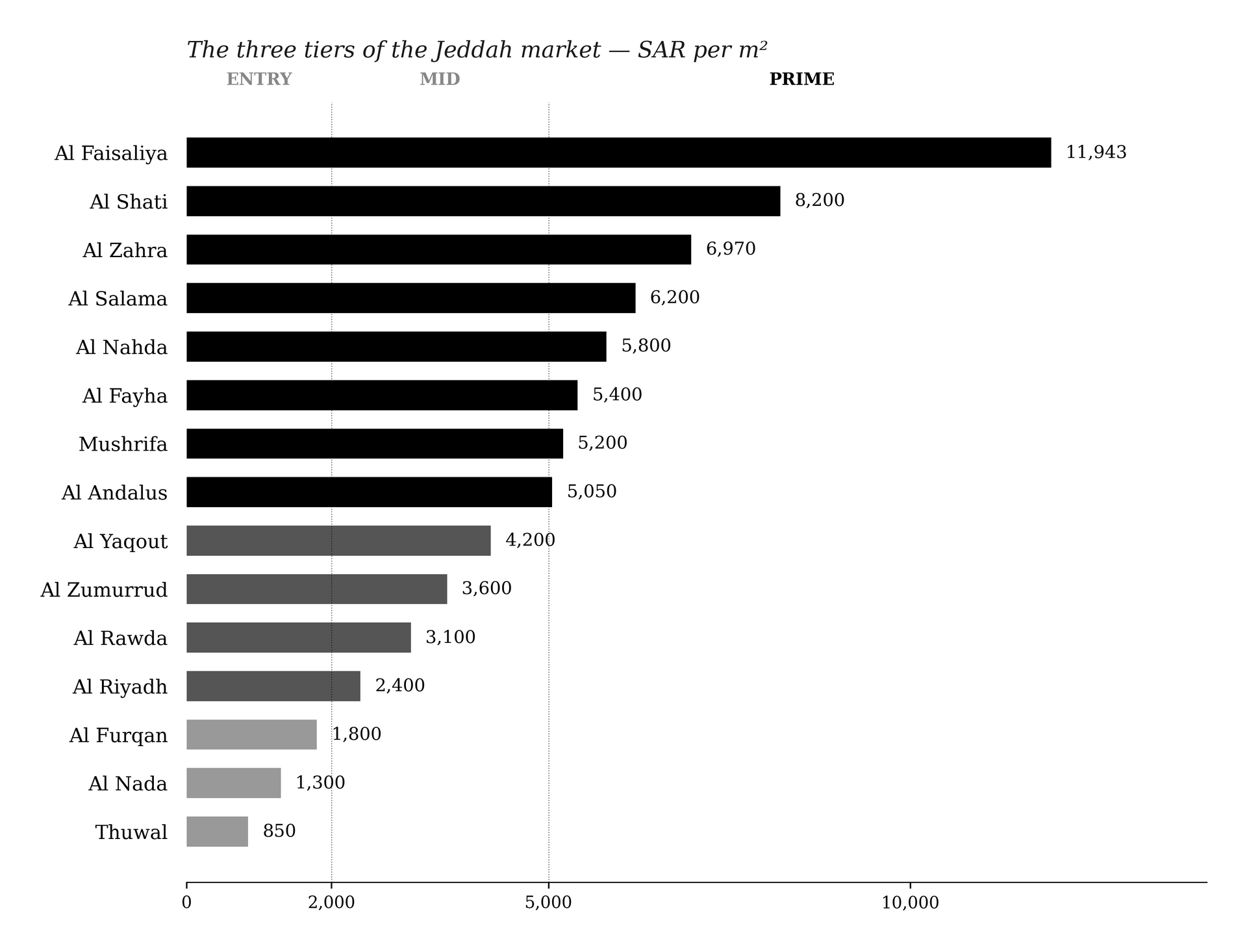

Three tiers, one city

Ranked by volume-weighted average price, the city's most active districts resolve into three distinct strata.

The prime tier — Al Faisaliya, Al Zahra, Al Salama, Al Nahda, Al Fayha, Mushrifa, Al Andalus — trades consistently above SAR 5,000 per square metre. This is the addressable territory for considered acquisition: the corridors where every metre commands a premium that reflects scarcity, location, and forward demand.

The mid tier — Al Yaqout, Al Zumurrud, Al Rawda, Al Riyadh, and similar — populates the SAR 2,000 to 5,000 band. Activity here is broader, frequently developer-led, and represents the bulk of city-wide residential land flow.

The entry tier — Thuwal, Al Nada, Al Furqan and similar peripheral districts — sits below SAR 2,000 per square metre. Volume is meaningful, but these are markets driven by end-user housing demand and speculative land banking rather than premium acquisition.

Three Jeddahs, transacting concurrently. The volume-weighted average price across all 984 transactions is meaningless to a buyer who intends to operate in the prime tier alone.

The quiet arrival of vertical luxury

Among the 456 apartment transactions registered in March, the headline figures are unremarkable: a median of SAR 500,000, a volume-weighted average of SAR 3,854 per square metre. The upper end of the registry tells a different story.

In Al Nahda, an apartment of 60.5 square metres registered at SAR 19,841 per square metre — the highest per-metre apartment price in the entire month, exceeding even Al Shati prime land in unit terms. In Obhur Al Janubiya, a 365-square-metre apartment cleared at SAR 13,970 per square metre, transacting at SAR 5.1 million in absolute value. In Al Salama, a 175-square-metre unit registered at SAR 9,571 per square metre.

These are not aberrations. They are the early signature of a vertical luxury market beginning to assert itself in Jeddah. Where buyers in the past sought scale through villa or land acquisition, a new cohort is electing height, finish, and view — and is willing to pay accordingly.

What we read from the month

Four observations follow from the data, offered to our clients in the spirit of clarifying rather than selling.

Commercial land at scale is the institutional story. The presence of multiple SAR 30-to-600-million commercial transactions in a single month signals continued institutional and corporate appetite for land aligned with Vision 2030 infrastructure, the foreign-ownership reforms that took effect in January, and the broader transformation of Jeddah's logistics and commercial axes.

The prime residential corridor is intact. Al Shati's SAR 19,800 per square metre benchmark, Al Faisaliya's commercial pricing power, and the persistent strength of Al Salama and Al Andalus collectively indicate that the most desirable Jeddah addresses are not following the softer national price index. The premium is being paid.

Vertical luxury has arrived as a serious category. The apartment registry now contains transactions that would have been unthinkable in Jeddah only two or three years ago.

And finally — the spread is the strategy. Jeddah is not a market into which one buys uniformly, but a market within which one selects with discipline. The relevant figure is never the city average; it is what the prime tier is doing. In March 2026, it is holding firm.

The full Q1 2026 Jeddah Market Intelligence brief — including the transaction-level dataset, district-by-district analysis, and the ten defining transactions of the month — is available to clients of TK Estate on request.

To request the brief, or to arrange a private consultation, write to us at

info@tk-estates.com